TL;DR Bitcoin's February 5th crash wasn't driven by crypto panic selling. Despite a 13.2% drop, Bitcoin ETFs recorded record inflows of $530 million, while Wall Street's risk-management systems forced broad deleveraging across all assets.

Record-Breaking Volume Masked the Real Story

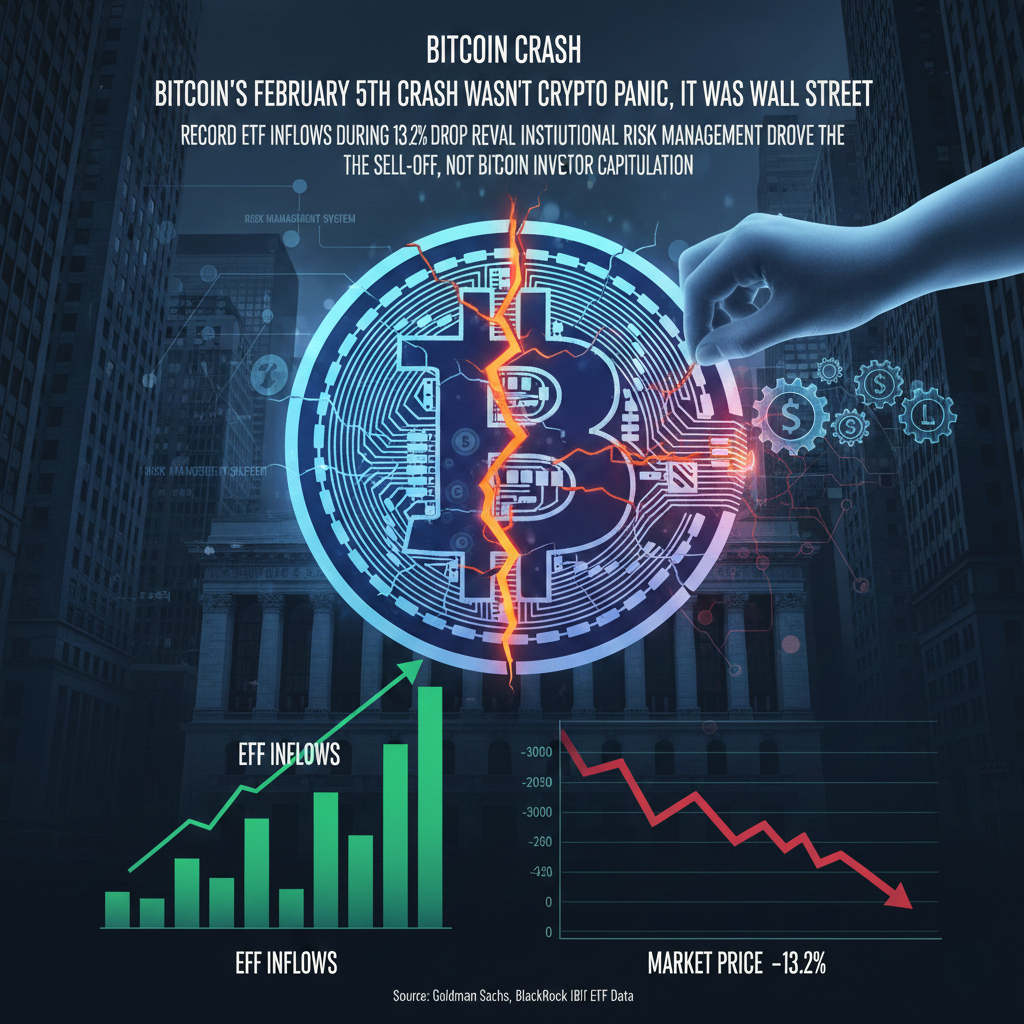

On February 5th, Bitcoin experienced one of its sharpest single-day drops in recent memory, falling 13.2% in a move that sent shockwaves through the market. The natural assumption? Crypto investors were bailing. But a closer examination of the data reveals a very different narrativeone where traditional finance was the primary culprit, and Bitcoin holders actually stood firm.

BlackRock's IBIT ETF hit record trading volume that day, exceeding $10 billion, double its previous all-time high. Options activity also reached the highest contract count since the ETF launched, with roughly 80% concentrated in put options betting on further downside. By every surface-level metric, this looked like capitulation.

The twist: despite the 13.2% drawdown, IBIT actually saw net inflows. Around 6 million new shares were created, adding over $230 million in assets. The broader Bitcoin ETF complex added another $300 million on top of that, bringing total inflows to $530 million. Historical precedent suggested we should have seen $500 million to $1 billion in outflows; the exact opposite occurred.

Wall Street's Risk Management Machine Goes Haywire

According to data from Goldman Sachs, February 4th was one of the worst single-day performance events for multi-strategy hedge funds in recent history. These firms manage highly leveraged portfolios often at 4.5x leverage across multiple asset classes. Goldman measured the day at a z-score of 3.5, making it a 0.05% probability event, ten times rarer than a standard three-sigma shock.

When losses that extreme hit funds managing billions with excessive leverage, risk managers don't discriminate; they issue blanket orders to reduce exposure across all positions. Bitcoin, now deeply embedded in institutional portfolios through Bitcoin ETFs that have seen massive growth, got caught in this indiscriminate selling wave.

The sell-off wasn't investors choosing to dump Bitcoin. It was automated risk reduction sweeping through every asset in these portfolios simultaneously. IBIT's price moved in near-lockstep with software stocks during the drawdown, confirming that selling pressure was broad and systematic rather than crypto-specific.

Options Markets Amplified the Carnage

What transformed a bad day into a bloodbath was the options market dynamics. Many dealers sold put options on Bitcoin at relatively low implied volatilities and were severely exposed when the market moved against them. As Bitcoin's price declined, those dealers were forced to sell IBIT shares to hedge, which further depressed prices, creating a self-reinforcing downward spiral.

Simultaneously, the CME Bitcoin basis trade, a popular arbitrage strategy among hedge funds, involved buying spot Bitcoin while selling futures, which was being aggressively unwound. The near-dated basis jumped from 3.3% to 9% in a single day, representing one of the largest moves since the ETF launched. Sophisticated trading firms that were likely running these strategies at scale were forced to sell spot holdings as part of the unwinding process.

The Recovery Revealed Bitcoin's True Strength

By February 6th, Bitcoin had snapped back more than 10%, demonstrating remarkable resilience. The basis trade quickly reconstituted as traders re-entered at more attractive spreads, and traditional finance normalized. However, the crypto-native side showed different behavior: Binance open interest collapsed, suggesting that crypto-native leveraged positions were liquidated and didn't return as quickly.

This divergence is telling. ETF buyers, the long-term, allocation-style investors that asset managers have been targeting, actually bought the dip. The recent ETF outflows we've seen appear to have been temporary, with institutional appetite remaining strong during actual market stress.

Integration Creates Both Risk and Opportunity

Bitcoin is now deeply woven into the traditional financial system through ETFs, custody solutions, and institutional adoption. This integration cuts both ways: Bitcoin can get swept up in broad deleveraging events that have nothing to do with crypto fundamentals, as evidenced by the February 5th crash occurring alongside broader market volatility affecting mining stocks.

However, this same integration means that when market mechanics eventually reverse direction, the same forces that accelerated the downside will likely amplify upside moves. The fragility of Wall Street's margin requirements and risk management systems may ultimately prove to be Bitcoin's greatest catalyst for explosive moves in both directions.

What This Means for Bitcoin Investors

The February 5th crash offers several key insights for Bitcoin investors and users of financial services:

For ETF Investors: Inflows during the crash support the thesis that ETFs provide access to patient capital that views volatility as an opportunity rather than a risk.

For Active Traders: Understanding that institutional risk management can create temporary but severe dislocations provides opportunities for those with dry powder and strong risk management.

For Service Selection: Events like these highlight the importance of choosing established custody and lending platforms that can weather institutional volatility without forced liquidations.

The crash wasn't a rejection of Bitcoin; it was Wall Street's internal plumbing causing temporary chaos in an otherwise resilient market. As institutional adoption continues to grow, understanding these dynamics becomes increasingly crucial for navigating Bitcoin's evolving market structure.