TL;DR Fidelity Investments launched the Fidelity Digital Dollar (FIDD) stablecoin on February 4, 2026, with $59 million initial supply and $60 million first-day trading volume. This marks a pivotal moment as one of the world's largest asset managers officially enters the stablecoin market under new federal regulations.

Traditional Finance Goes Full Crypto

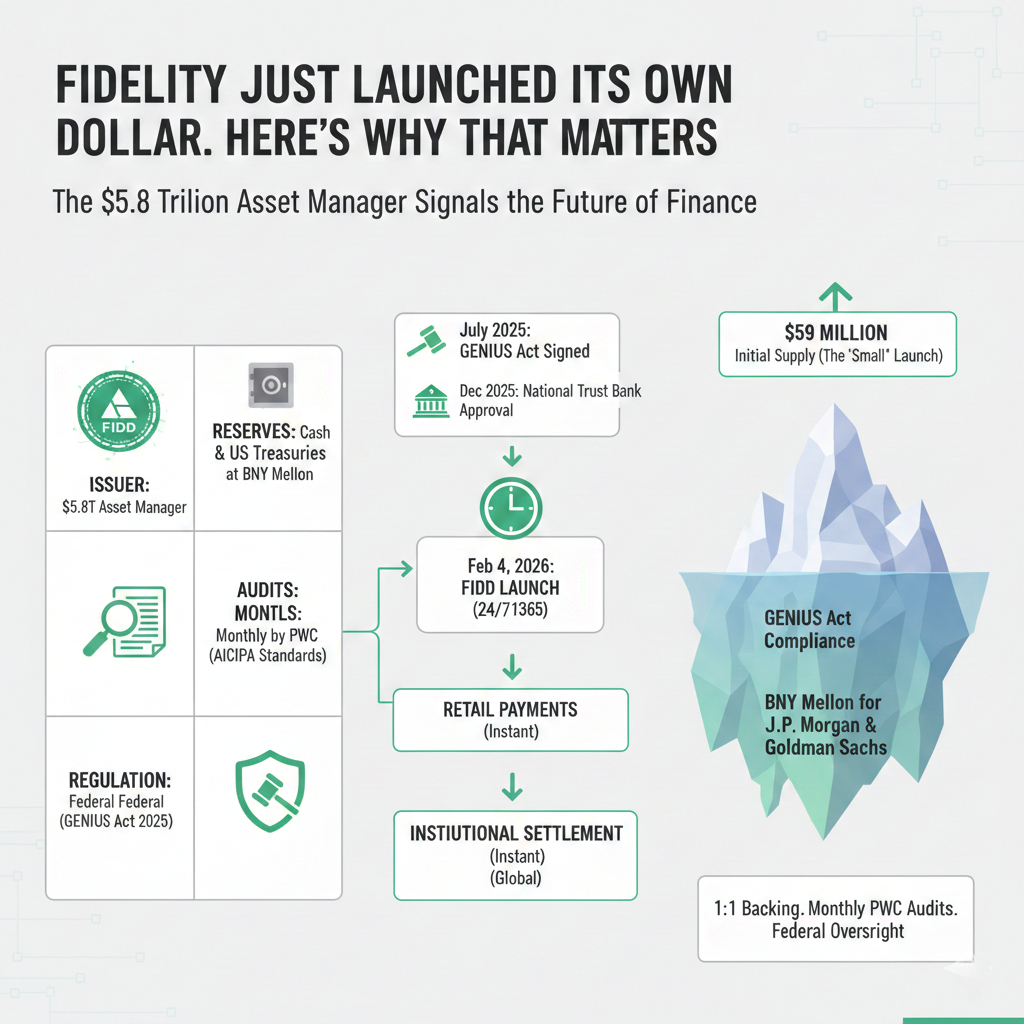

On February 4, 2026, Fidelity Investments crossed a line that few traditional financial institutions have dared to approach: issuing their own digital currency. The Fidelity Digital Dollar (FIDD) launched on Ethereum with over $59 million in initial supply and cleared $60 million in daily trading volume on day one.

This isn't a crypto startup experimenting with tokenized money. This is a $5.8 trillion asset manager, one of the largest financial institutions globally, creating its own stablecoin backed by the same rigorous infrastructure that manages millions of retirement accounts.

The timing coincides with broader institutional adoption trends we've been tracking, including recent Bitcoin ETF developments and Wall Street's evolving crypto stance.

What Makes FIDD Different

FIDD operates like other major stablecoins; one token equals one dollar, redeemable at any time. The critical difference lies in the institutional backing and regulatory compliance framework.

The stablecoin is issued by Fidelity Digital Assets and fully backed by cash, US Treasuries, and highly liquid assets held in custody at Bank of New York Mellon. Reserve management is within Fidelity Management & Research Company, the same division that oversees the firm's massive mutual fund operations.

Transparency measures exceed current industry standards: Fidelity publishes FIDD's circulating supply and reserve net asset value daily at market close. Monthly reserve reports are examined by PricewaterhouseCoopers under AICPA attestation standards, a level of oversight that most existing stablecoins haven't matched.

Regulatory Framework Enables Launch

The timing isn't coincidental. The GENIUS Act, signed into law in July 2025, established the first comprehensive federal regulatory framework for payment stablecoins in the United States. This legislation created clear rules around reserve requirements, transparency standards, and issuer qualifications.

The Office of the Comptroller of the Currency granted Fidelity Digital Assets conditional approval to operate as a national trust bank in December 2025, clearing the final regulatory hurdle.

Mike O'Reilly, president of Fidelity Digital Assets, called the GENIUS Act "a key enabler" and noted the firm spent years researching stablecoins before determining the regulatory environment was sufficiently mature.

Market Positioning and Use Cases

FIDD launches across Fidelity's own platforms, Fidelity Crypto and Fidelity Crypto for Wealth Managers, while maintaining transferability to any Ethereum address. This approach enables usage across decentralized finance protocols and third-party exchanges upon listing.

Primary use cases target institutional settlement (enabling 24/7 trade settlement versus traditional banking hours) and on-chain payments for retail users. Fidelity indicated potential expansion to additional blockchains and layer-2 networks in future phases.

For Bitcoin investors specifically, FIDD could streamline trading pairs and settlement processes across exchanges, potentially reducing friction in Bitcoin lending platforms like Arch Lending, Unchained, and Ledn.

Stablecoin Market Implications

The broader stablecoin market currently sits at approximately $316 billion, with Tether's USDT commanding nearly 60% market share and Circle's USDC holding most remaining volume. FIDD's $59 million launch represents a small fraction initially.

However, the significance transcends initial numbers. Fidelity becomes among the first major traditional financial institutions issuing stablecoins under the new federal framework. Market analysts expect J.P. Morgan, Goldman Sachs, and other major banks to follow with competing tokenized dollar products throughout 2026.

Infrastructure for Financial Evolution

When a firm managing $5.8 trillion in assets decides to issue its own digital currency, it signals infrastructure building rather than trend chasing. This development signals a shift toward a financial system where settlement occurs instantly, markets operate continuously, and distinctions between traditional and digital finance blur significantly.

For Bitcoin and cryptocurrency users, institutional stablecoin adoption like FIDD could enhance liquidity, reduce counterparty risks, and provide more reliable on-ramps and off-ramps for digital asset trading and custody solutions.

As traditional finance continues embracing digital assets from Bitcoin ETFs to mining company partnerships, Fidelity's FIDD launch marks another milestone in the ongoing convergence between legacy financial institutions and cryptocurrency infrastructure.