TL;DR - Bitcoin-backed loan rates dropped from 12-15% to as low as 4% APR in two years. Competition from DeFi (Coinbase/Morpho) and new entrants (Strike) crushed pricing. But rate isn't the only variable - custody model, fee structure, and liquidation terms vary wildly. We compared 8 platforms on what actually matters.

Why 2026 Is Different for Bitcoin Lending

Two things changed the lending landscape this year.

First, competition drove rates down. In 2022, borrowing against Bitcoin cost 12-15% APR from the few surviving lenders. Today, rates start around 7-8% APR from regulated platforms, and Coinbase's on-chain product via Morpho can get as low as 4%. More lenders, more capital, lower prices.

Second, the 2022-2023 collapses permanently changed how serious borrowers evaluate platforms. Celsius, Voyager, and BlockFi all went bankrupt because they rehypothecated customer collateral - they took the Bitcoin people deposited as collateral and lent it out again to generate yield. When those bets went bad, borrowers' collateral evaporated.

The survivors - Ledn, Arch, SALT, Unchained - made it through specifically because they didn't do this. And the new entrants like Strike and Coinbase are building products with non-rehypothecation as a baseline feature, not a marketing differentiator.

If you're borrowing more than $50,000 against your Bitcoin in 2026, custody model matters more than interest rate.

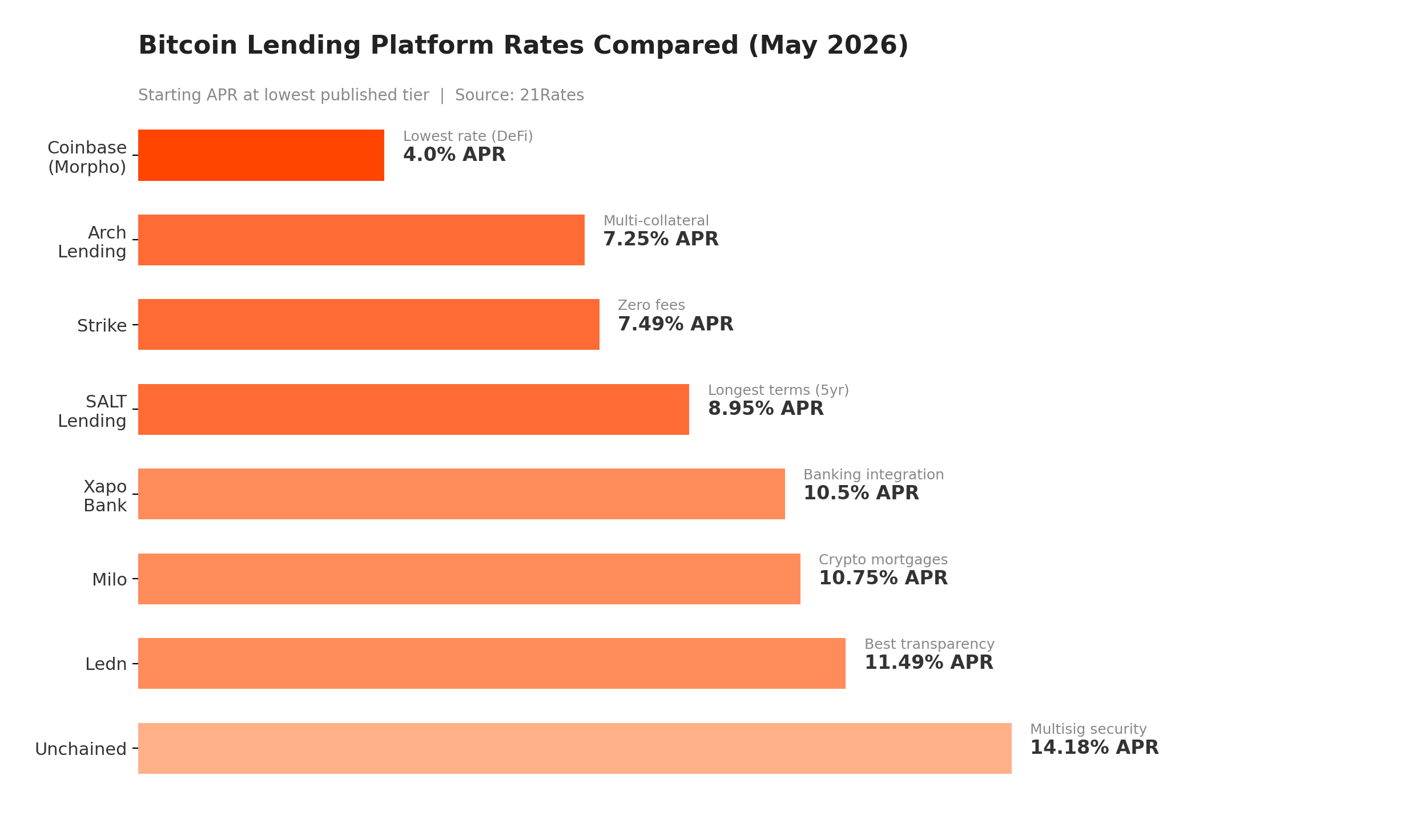

Bitcoin Lending Platforms Ranked by Rate

Here's every major platform ranked from cheapest to most expensive. Note that advertised rates often come with conditions - higher LTV tiers, larger loan sizes, or shorter terms can all shift the number you actually pay.

| Platform | Starting APR | Max LTV | Min Loan | Custody | Rehypothecation |

|---|---|---|---|---|---|

| Coinbase (Morpho) | ~4% variable | ~75% | Varies | On-chain (Morpho) | No |

| Strike | 7.49% | 50% | $10,000 | Qualified custodian | No |

| Arch Lending | 7.25% | 60% | $1,000 | Anchorage Digital | No |

| SALT Lending | 8.95% | 70% | $5,000 | Qualified custodian | No |

| Xapo Bank | 10.5% | 40% | $1,000 | Xapo Bank (licensed) | No |

| Milo | 10.75% | 50% | $100,000 | Coinbase / BitGo | No |

| Ledn | 11.49% | 50% | $1,000 | Custodied (no rehyp) | No |

| Unchained | 14.18% | 40% | $150,000 | 2-of-3 multisig | No |

Rates reflect published minimums as of May 2026. Actual rates depend on loan size, term, and LTV tier.

Top 6 Bitcoin Lending Platforms for 2026

Coinbase (via Morpho) - Lowest Rate, On-Chain Transparency

Coinbase's Bitcoin lending product runs through Morpho, a DeFi lending protocol on Base. You deposit BTC (or cbBTC), borrow USDC, and the entire position lives on-chain. No intermediary holds your collateral in the traditional sense - it sits in a smart contract.

The rate is the lowest in the market by a wide margin. Around 4% variable APR versus 8-14% at centralized lenders. The trade-off is that rates float with market conditions - during high demand, that 4% could spike.

The product reached $1.25 billion in borrowing volume by April 2026. But there's a DeFi risk here: smart contract risk. Morpho has been audited extensively, but "code is law" means there's no customer service line if something goes wrong.

Not available to New York residents. If you're comfortable with DeFi mechanics and want the cheapest rate, this is it.

Strike - Best for Zero-Fee Simplicity

Strike's pitch is simple: no hidden fees, anywhere. Zero origination fee. Zero prepayment penalty. Zero liquidation fee. In a market where most lenders charge a 2% origination fee on top of interest, this matters more than people realize. On a $250,000 loan, that's $5,000 out of your pocket before interest starts.

The rate structure is tiered: loans under $250K start around 10.5% APR, while loans over $5M can get as low as 7.49%. Once you factor in zero fees, the effective cost often beats lenders with lower headline rates.

Strike CEO Jack Mallers announced a "volatility-proof" loan structure at the Bitcoin 2026 Conference, built in partnership with Tether and backed by a $2.1 billion credit facility. The idea is to eliminate forced liquidation risk during price crashes. Details are still emerging, but if it delivers, it solves the single biggest anxiety Bitcoin borrowers have.

Arch Lending - Best for Flexible Collateral

Arch is where you go if you hold more than just Bitcoin. The platform accepts BTC, ETH, SOL, and XRP as collateral, and you can use multiple assets in a single loan.

The custody setup is the strongest in the centralized lending space. Anchorage Digital is a federally chartered digital asset bank. Your collateral sits in segregated wallets with an explicit no-rehypothecation policy and $100 million in Lloyd's of London insurance.

The 60% LTV is the highest among traditional CeFi lenders (excluding SALT's 70%). On a $500K loan at 50% LTV you need $1M in Bitcoin. At 60% LTV, that drops to $833K. The $1,000 minimum makes it accessible for smaller borrowers too.

Ledn - Best Transparency Track Record

Ledn isn't the cheapest option anymore, but it has the longest track record of not losing customer money. The platform has published semi-annual Proof of Reserves attestations since January 2021 - longer than any other crypto lender. A top-25 accounting firm verifies that all client assets are accounted for, and individual borrowers get anonymous verification codes to confirm their balance was included.

Rates are tiered: 11.49% under $250K, 10.49% for $250K-$1M, 9.99% for $1M-$2M, and 9.25% above $2M. The 2% admin fee for non-US borrowers is waived for US borrowers. No prepayment penalties.

SALT Lending - Longest Terms Available

SALT has been around since 2016, making it the oldest surviving Bitcoin lender. The standout feature is term length: 3-year and 5-year loans that nobody else offers. If you're borrowing against Bitcoin with a long time horizon and don't want to worry about annual refinancing, this is your only option.

The 70% LTV maximum is the highest in traditional CeFi. That's aggressive - a ~30% price drop could trigger margin calls. The rate range is wide: 8.95% at the floor, but push to 70% LTV on a longer term and you're looking at 15%+ APR.

Unchained - Best Security, Highest Cost

Unchained charges 14.18% APR, requires $150,000 minimum, charges a 2% origination fee, and only lends to business entities. Individuals can't borrow here.

The reason: the 2-of-3 multisig custody model. You hold one key, Unchained holds one, and an independent third party holds the third. Nobody can move your Bitcoin unilaterally. You can verify your collateral on-chain at any time. This is the only lending product where the borrower retains partial custody during the loan.

How to Choose the Right Bitcoin Lending Platform

How much are you borrowing? Under $50,000, your options are Arch ($1K min), Ledn ($1K), SALT ($5K), or Strike ($10K). Over $150K, Unchained enters the picture for business borrowers. Over $1M, tiered rates at Ledn and Strike start working in your favor.

How long do you need the money? Most loans are 12-month terms. SALT's 5-year is unique. Coinbase's Morpho has no fixed term.

How much do you care about custody? Unchained's multisig is the gold standard. Arch's Anchorage arrangement with $100M insurance is next. Coinbase eliminates the custodian via DeFi (but introduces smart contract risk).

One rule for everyone: ask what happens to your collateral during the loan. If the answer isn't "nothing," use someone else.

For more, see the 21Rates Lender Comparison and our Bitcoin Custody Guide.

Frequently Asked Questions

What happens to my Bitcoin if the price drops during my loan?

If Bitcoin's price falls far enough that your loan-to-value ratio exceeds the platform's threshold, you'll get a margin call. Most platforms give you 24-72 hours to add more collateral or make a partial repayment. If you don't, they'll sell enough of your Bitcoin to bring the LTV back in line. Always know your liquidation price before you borrow.

Do Bitcoin-backed loans trigger a taxable event?

No. Borrowing against your Bitcoin is not a sale, so it doesn't trigger capital gains tax under current US tax law. This is the primary reason people use Bitcoin-backed loans. However, if you get liquidated, that is a taxable event. For more on crypto tax rules, see our crypto tax software comparison.

What's the difference between rehypothecation and non-rehypothecation?

Rehypothecation means the lender takes your deposited Bitcoin and lends it to someone else. This is what destroyed Celsius, BlockFi, and Voyager. Non-rehypothecation means your Bitcoin stays put in custody, untouched, until you repay. Every platform in this guide has a non-rehypothecation policy.

Which platform is best for large loans over $1 million?

For rate: Strike drops to 7.49% above $5M and Ledn goes to 9.25% above $2M. For security: Unchained's multisig is purpose-built for large positions. For DeFi: Coinbase/Morpho has processed over $1.25B in volume. For real estate: Milo handles crypto mortgages up to $25M.

Can I get a Bitcoin-backed loan without a credit check?

Yes. All platforms in this guide use Bitcoin as the sole underwriting criterion. No credit check, no income verification. The collateral is the underwriting.

How do Bitcoin loan rates compare to traditional loans?

Bitcoin-backed rates (7-14% APR) sit between personal loans (8-15% from banks) and margin loans on stock portfolios (5-9% at major brokerages). For holders who want to avoid selling, the after-tax cost can actually be lower than selling and rebuying.

This article is for informational purposes only and does not constitute financial or investment advice. Bitcoin-backed loans carry liquidation risk. Consult a qualified financial advisor for your specific situation.

Sean Ristau | @SeanRistau | 21Rates / The Daily Stack